It may come as no surprise that UK businesses are holding on to their cash where they can at the moment.

Recent research we conducted at Wow shows that 37% of businesses with 5-75 staff currently hold more than six months running costs as cash in the business. Cash balances have never looked better with only 9% of businesses reporting they have one month or less of running costs as cash in the bank.

Big increase since January

There has been a big increase in cash reserves since the start of the year. In research we conducted at the start of January, nearly twice as many businesses (17%) reported being close to the brink.

Too good to be true?

Six months later, one global pandemic and an economic meltdown later, businesses have more cash in the bank. On the face of it, this is cause for optimism, and maybe it is.

The latest government data shows:

- 1,100,000+ businesses have taken out Bounce Back or CBILS loans totalling £45bn

- 1,200,000 businesses have been able to furlough staff on reduced pay and have the government pick up the wage bill

- Businesses have also been able to defer VAT payments until next year

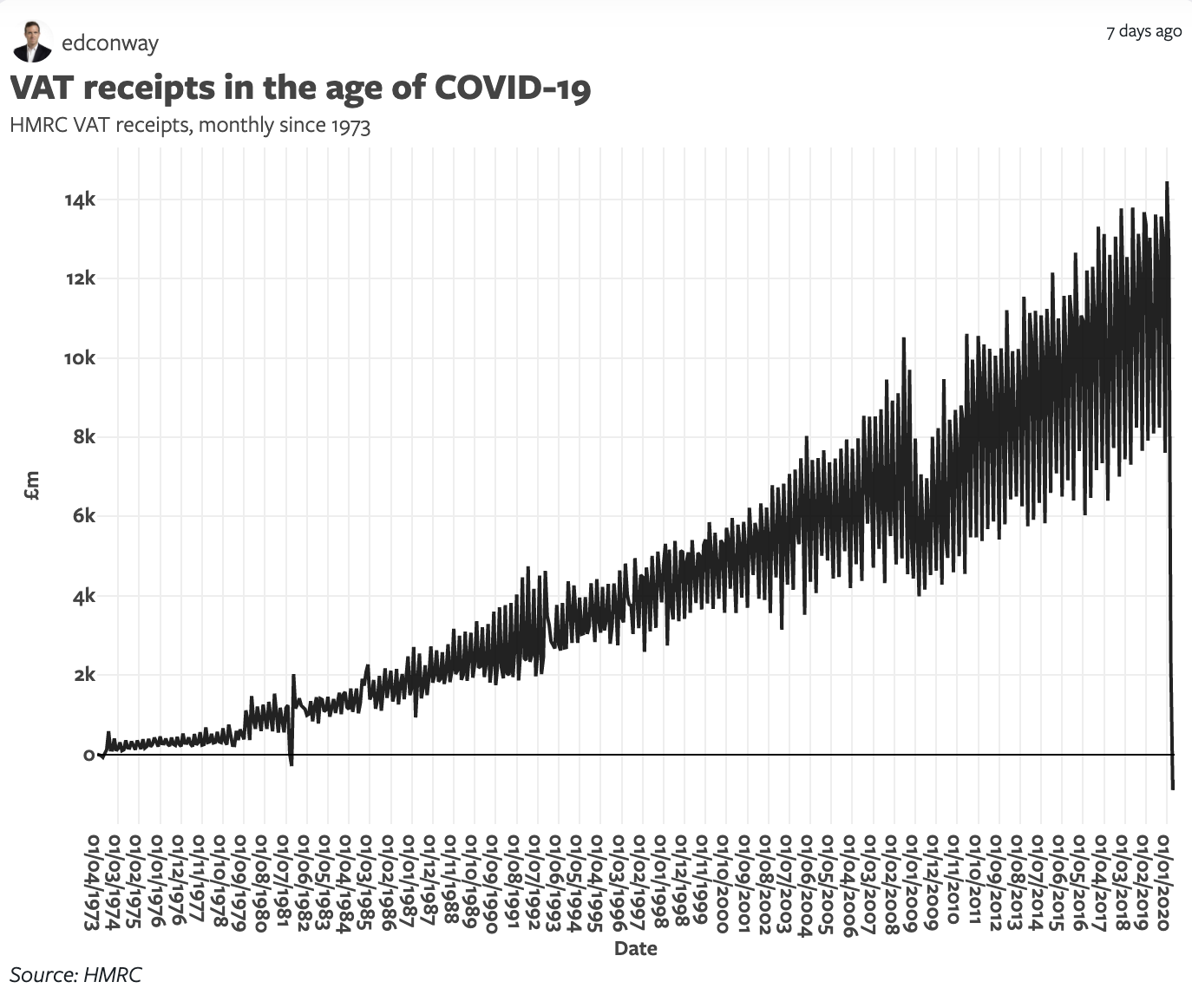

HMRC released data showing that for the first time since the tax was introduced in 1973, there have been ‘negative’ VAT receipts – meaning they have repaid more than they have received. Whilst some of this dip reflects the dramatic halt in economic activity, VAT receipts are by definition lagging as the returns and payments don’t have to be paid until a month after the end of the quarter. Much of this dip is probably down to VAT deferments.

Borrowed time?

HMRC has allowed businesses to defer their VAT payments en masse, looking at this chart you can get an idea of the amount of VAT (i.e. cash) that will have to be repaid (in theory) by 31st March 2021. These VAT repayments will fall due at roughly the same time as businesses have to start repaying their Bounce Back or CBILS loans. As the furlough scheme unwinds over the coming months, there’s another cash hit arriving sooner as businesses have to either start paying their staff themselves or stump up the cash for redundancy payments.

It’s encouraging to see the increased cash balances being held in businesses, and there definitely is a cause for optimism. Not least because businesses will have more resilience to cope with what comes ahead. It’s a reasonable assumption that cash balances are borrowed in one way or another at the moment. If that cash is being put aside to protect against what might come next – great. But, if this cash is being used now as working capital, some businesses may get into trouble when it comes to paying it back.

Wow’s advice

- Transfer the cash for any tax payments you’ve deferred to a separate bank account if you can. Try not to live off that cash now unless you absolutely have to.

- Keep your own cash flow forecast – even if it’s very basic. A cash flow forecast will give you some visibility over what cash you’re going to need to operate in the coming weeks or months. This will be especially important if you have to make loan repayments and repay deferred taxes at some point next year.

- If you notice your cash levels dipping, take action. Don’t wait until it’s too late. If you’re concerned at all, please come and talk to us.