The new inheritance tax rules will make passing on your estate a lot easier and less costly from 6 April 2017. Your estate is the sum of your savings, investments, settled property, the market value of the house you live in and other assets less any available reliefs, outstanding debts and reasonable expenses.

Every individual already has a £325,000 threshold for their estate that is not subject to inheritance tax. From 6 April 2017 in addition to this threshold – the residence nil-rate band (RNRB) – can be claimed by the estates of people who die on or after 6 April 2017.

Who qualifies for the new inheritance tax rules?

The RNRB will apply to an estate if an individual leaves a home to their children or other direct descendants when that individual dies, on or after 6 April 2017.

The estate must contain a house that has been used as the individual’s private residence. They don’t have to be living in the property at death.

The individual can leave their home to their children, grandchildren, great grandchildren and so on either by will or intestacy. This also includes their step-children, adopted children, foster children or a child for whom the individual was a guardian when the child was under 18.

The person who inherits the property doesn’t need to live in the property after the individual’s death.

Amount of relief for the RNRB

The amount is the lower of two options:

- Net value of the qualifying residence – this is the value of the residence at death less any liabilities secured on the property, or

- The RNRB amount which is:

- £100,000 in 2017/18

- £125,000 in 2018/19

- £150,000 in 2019/20

- £175,000 in 2020/21

This will increase in line with the Consumer Price Index (CPI) from 2021 to 2022.

If the property is worth less than the RNRB then the excess cannot be used against the rest of the estate.

RNRB limitations

There’s a limitation of one residential property per estate. There’s no minimum ownership period, but a property that has never been a residence of the deceased will not qualify.

For estates over £2 million, the RNRB is tapered away by £1 for every £2 over the limit.

Unused RNRB

Any unused RNRB can be transferred to the deceased’s spouse or civil partner. This also applies if the first person died before 6 April 2017.

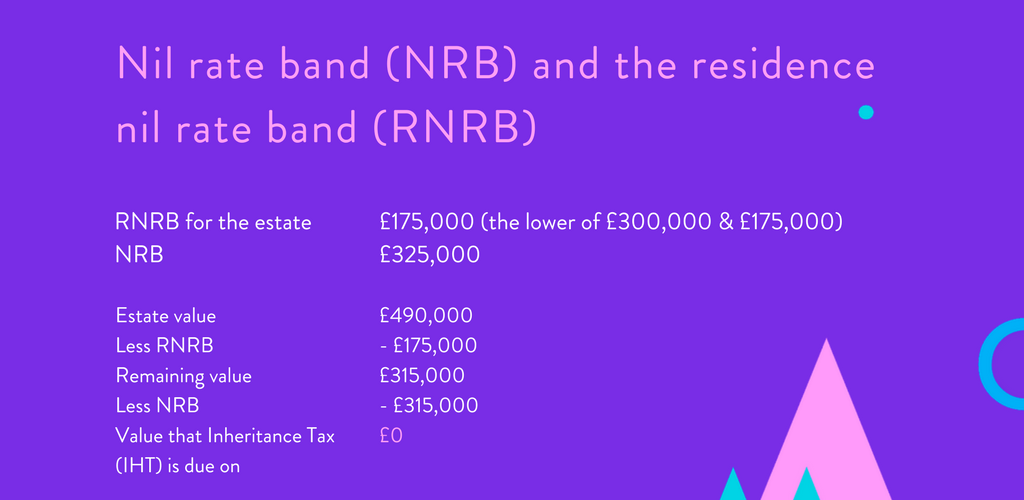

How to calculate and apply RNRB

Mr A dies in the tax year 2020/21 and leaves a home worth £300,000, and other assets worth £190,000 to his children.

The maximum available RNRB in tax year 2020/21 is £175,000. In this example, we would be applying both the nil rate band (NRB) and the RNRB to the estate.

In this case, the whole of the RNRB has been used up. The unused percentage of his NRB will be available to his wife on her death.

If you would like more information or to discuss how this may impact you please contact me:sarah.eble@thewowcompany.com.